In the high-stakes world of medical supply distribution and Durable Medical Equipment (DME), your cash flow is the lifeblood of your operations. When hospitals, private clinics, or surgical centers fall behind on invoices, it’s more than just a late payment—it’s a disruption to the healthcare supply chain.

Collection Agency USA (CA-USA) offers a specialized, clinical-first approach to medical supply debt. We understand that in this industry, reputation is everything; today’s delinquent account could be tomorrow’s most vital partner.

Need a Collection Agency? Contact us

Why Medical Suppliers Trust CA-USA:

-

Clinical, Not Combative Methodology: Our agents treat your debtors like the medical professionals they are. We use a firm, fact-based approach that secures payment while preserving your long-term business relationships.

-

National Licensing & Compliance: With licenses in all 50 states and SOC 2 Type II compliance, we ensure your data and your reputation are protected under the highest security standards.

-

Skip-Tracing for “Ghost” Practices: Private practices often merge or close unexpectedly. Our elite skip-tracing databases locate responsible parties and personal guarantors, even after they’ve moved or rebranded.

-

Strategic Credit Reporting: We provide the necessary leverage by reporting unresponsive B2B accounts to major bureaus, motivating payment before their ability to secure future inventory is compromised.

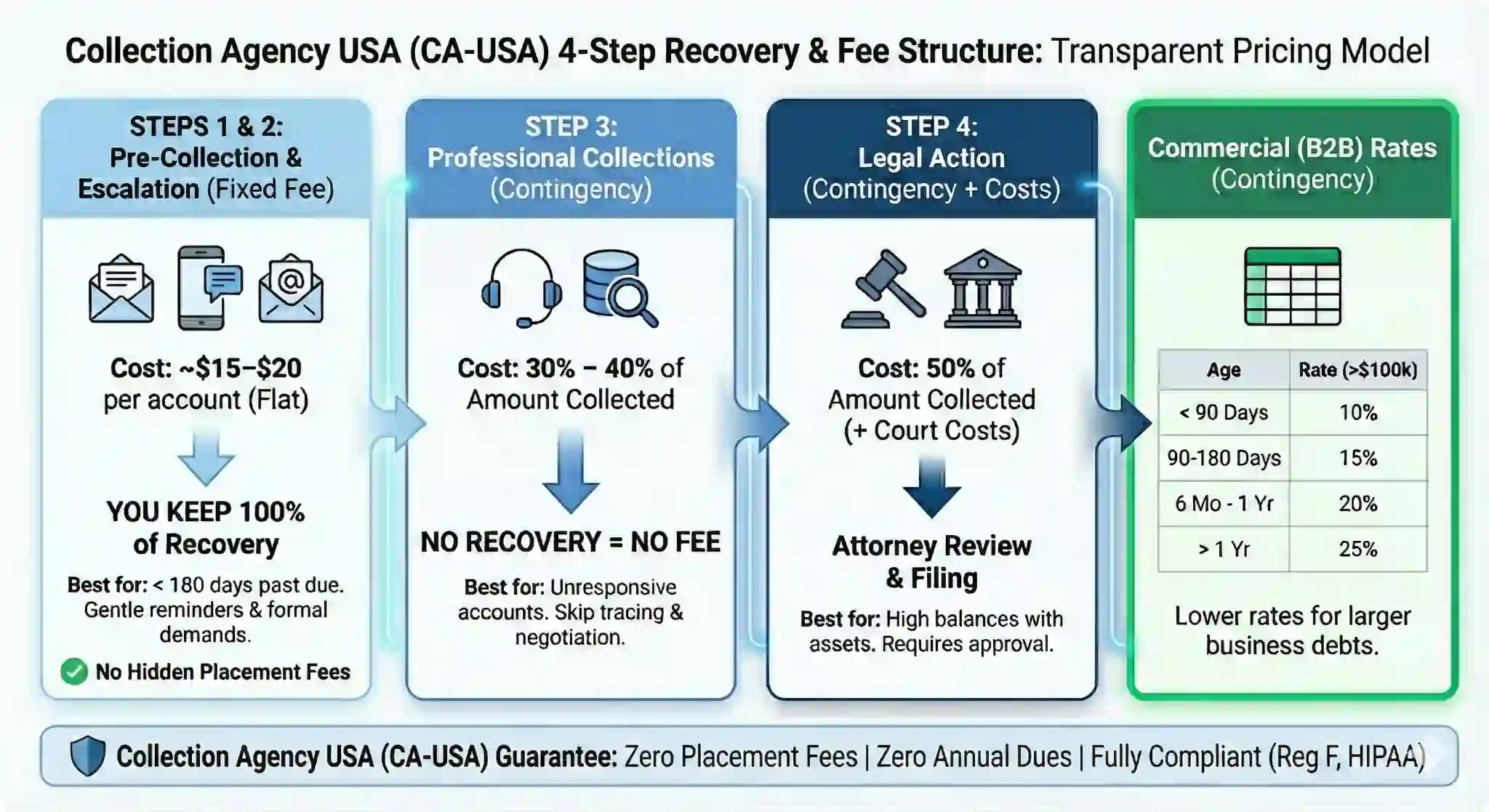

Performance-Driven Pricing:

-

Fixed-Fee: $15 per account (Keep 100% of the recovery).

-

Contingency: 40% (No recovery, no fee).

Frequently Asked Questions: Medical Supply Debt Recovery

Do you handle both B2B and B2C collections?

Yes. We specialize in nationwide recovery for both B2B accounts (hospitals, surgical centers, and private practices) and B2C accounts (individual patients and home-care clients). Whether you are dealing with a bulk invoice or a single patient balance, we have the infrastructure to manage it.

How do you protect our reputation with healthcare providers?

We maintain a 4.85/5-star Google review ranking from over 2,000 professional reviews. This reflects our “Clinical, Not Combative” approach. We resolve disputes through professional mediation and factual evidence, ensuring your professional relationships remain intact while the balance is settled.

Is CA-USA compliant with healthcare privacy standards?

Absolutely. We are fully SOC 2 Type II compliant and adhere to all national debt collection regulations. Our systems are built to handle sensitive medical billing data with the highest level of security and discretion.

Can you find medical directors or facility owners who have “disappeared”?

Yes. Our deep-data skip-tracing tools allow us to locate personal guarantors and business owners even if a practice has closed or moved. We find the responsible parties that standard searches miss.

What is the benefit of your nationwide reach?

Medical supply chains often cross state lines. Because we are licensed and bonded nationwide, we can pursue debtors anywhere in the U.S., providing a single-source solution for your entire accounts receivable portfolio.

How does credit reporting help in this industry?

For B2B accounts, a collection mark on a business credit report can hinder their ability to secure future inventory or financing. This provides significant leverage, often resulting in payment without the need for litigation.

Hire a Collection Agency? Contact us

Protect your margins without sacrificing your professional standing. Partner with CA-USA for medical supply debt recovery that works as hard as you do.